Steve Ballmer explains the Federal Reserve

The Federal Reserve may be the most important bank you never use. But why is it called a “bank”, how is it governed, and how does it influence daily life in the US? In this episode of Just the Facts, Steve Ballmer tells you everything you need to know about the Federal Reserve Bank of the United States.

Up Next

Transcript

Steve: Headlines are always talking about the Fed. The Fed raised rates. The Fed cut rates. The Fed is fighting inflation. Most people don't interact directly with the Fed. That is, the Federal Reserve Bank. You don't walk into a Fed branch to open a checking account or make a withdrawal. Bonnie and Clyde never stormed the Fed.

But Fed decisions can make your car payments more expensive, your mortgage cheaper, or a job harder to find. So, let's take a closer look at the Federal Reserve, the central bank of the United States. What is it? Who runs it? And why was it created?

Steve: I'm Steve Ballmer and this is Just the Facts. Data-driven facts to help you make up your own mind. In this episode: the Federal Reserve.

It was created after a series of financial panics, especially the Panic of 1907, which led to runs on banks and one big mess. A run on a bank is when lots of customers all try to withdraw their money at the same time from their regular, everyday banks, the ones you and I use. Even a healthy bank can run out of cash if that happens. So in 1913, Congress passed the Federal Reserve Act.

It's the most important bank you'll never actually use. So why is it even called a bank? Because it's a bank for banks. It holds cash reserves for banks. It moves money between banks. And it can lend to banks whenever needed.

Today, the Fed has five core responsibilities. First, conduct the nation's monetary policy to keep inflation in check and employment high. Second, keep the financial system stable by preventing crises like bank runs, by lending money to banks so they can keep operating. Third, supervise certain financial institutions like banks and savings and loans. Fourth, foster payments and settlement systems like wiring money. And fifth, promote consumer protection. The last three make sure the financial system works and plays by the rules.

Alexander Hamilton: I started a national bank, but never a central bank. That's impressive.

Steve: I'm going to focus most on number one, monetary policy, because that's where the Fed most directly affects your wallet. Here's a big reason why: the Fed can influence interest rates. I'll explain how in a minute, but here's what it means.

The Fed can run the economy hot by working to lower interest rates. That can make buying a house, getting a car loan, or borrowing to open a business less expensive. The problem with hot is it may make money easier to borrow, which may fuel inflation.

The Fed doesn't raise your interest rates directly. It raises or lowers its target range for what is known as the federal funds rate.

Or the Fed can run the economy cold by raising interest rates. All those things become more expensive. The problem with cold is it may make money harder to borrow, which can slow the economy down and could have a lot of secondary effects, such as higher unemployment.

So exactly how does all that happen? The Federal Reserve doesn't raise your interest rates directly. It raises or lowers its target range for what is known as the federal funds rate.

Whoa. Whoa. Jargon warning. Federal funds range. What's that mean?

Banks move money between each other every day as customers withdraw or deposit money. By the end of the day, some banks have extra cash, while others don't have enough. Banks with extra money lend it overnight to other banks that need it at a rate within a range that the Fed sets.

How does the Fed drive banks to lend within this range? In simple terms, the Fed changes the interest on loans it gives and on other banks' cash reserves it holds, effectively setting the floor and the ceiling at which other banks can charge interest. Banks generally won't lend for less than they can earn from the Fed, and they usually won't borrow from other banks for more than what the Fed itself would lend to them. The average of overnight transactions between banks is called the federal funds rate.

The Federal Reserve lowered the federal funds rate. It sits between 3.5% and 3.75%.

Federal funds effective rate, by month

So let's dig deeper on the federal funds rate and how it can affect you. When the Fed raises the federal funds range, your bank may raise interest rates on new loans because their costs are going up. Higher rates make mortgages, car loans, credit cards, and short-term business loans more expensive.

There can then be a domino effect. Because mortgages are more expensive, people could be less likely to buy a home. Fewer home sales could mean less spending on things like moving, furniture, and home improvement. That slowdown in spending can ripple through the economy.

When this happens across the whole economy, people might spend less money because things are more expensive. Then inflation can decrease because demand falls. And as demand decreases, companies may need fewer workers, and often unemployment rises.

That's economics 101. Higher interest rates can mean lower demand for certain products, and that can cut inflation. But it can also mean more unemployment. This is not an exact science. The economy is complex, with many influences: tax policy, wars, oil prices, consumer sentiment, innovation, and more. At USAFacts, we do not forecast.

Now, let's look at another possible outcome. When the Fed lowers the federal funds range, the interest rates you pay from your bank can sometimes go down. In this case, for example, new car loans are cheaper and more people can afford to buy cars. Auto producers make more cars. And with more demand for those products, prices can increase, which means more inflation.

Congress tasks the Fed with what's called a dual mandate: to try to keep stable prices and maximum employment. That's a balance. Think of the economy like something in the oven, and the Fed controls the temperature. If things start overheating, prices rise too fast. The Fed turns down the heat. If things cool off too much, growth slows, jobs disappear, and the Fed turns the heat up. The goal is to keep the economy baking just right.

No Katy Perry. When it's hot and it's cold, you're yes and you're no. None of that!

Pretty good.

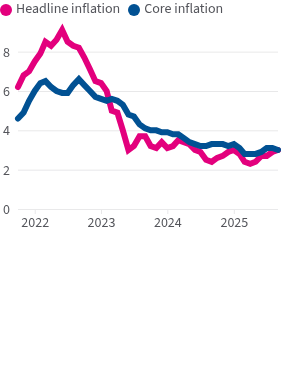

Over the last decade, the Fed has changed the federal funds rate target range about 30 times. Some years, like 2021, there were no changes at all. Other years move quickly. In 2022, the Fed raised rates seven times in a single year.

Well, why? The Fed aims for about 2% inflation over time. In 2022, inflation climbed well above the Fed's 2% goal, reaching about 7%. In response, the Fed raised the federal funds target range multiple times in 2022 and 2023. Short-term interest rates rose, car loan and mortgage rates increased, economic growth slowed, and inflation eventually slowed. It's not a perfect cause and effect, but the Fed's actions can influence the direction of inflation.

Now let's take a look at an example of lowering interest rates. In March 2020, as the COVID-19 pandemic disrupted economic activity and unemployment rose very sharply, the Fed lowered the target range for the federal funds rate to 0% to 0.25%. Very near zero.

Now stay with me. I got one more big thing. Sometimes the Fed uses other monetary policy tools when changes in interest rates are not enough. One big one is called open market operations.

Remy: Wait a second, that makes no sense.

Steve: Sorry, it's the nerd in me. Open market operations are just how the Fed puts money into the economy and how it takes money out of the economy.

Remy: That doesn't help. Give me an example.

Steve: Good question. Banks hold government bonds that they have bought as an investment. The Fed goes to the bank and buys the bonds. When it does that, it pays the banks, basically giving them more money.

Remy: Where does the Fed get that money?

Steve: You got questions? I got answers. The Fed creates it electronically, not with a printing press, just numbers on a screen. The Fed is unique that way. It can actually increase the supply of money.

In this example, the end result is simple. Now, banks have more money, so they can lend more money.

Remy: How does it help people?

Steve: Another good question. It can help a lot. More lending can mean lower interest rates, so it's cheaper to borrow for things like homes or businesses, or a skateboard and a helmet. The Fed did this a lot during COVID-19 to keep money flowing and borrowing costs low.

Remy: Open market operations. I've got it. You're not going to quiz me, are you?

Steve: Nah, you already got an A for just listening.

Federal Reserve assets have exceeded $6T since April 2020.

Federal Reserve total assets, Dec 2002–May 2026

So now that we have info on what the Fed does, let's talk about who exactly these people are and how the bank is organized. They are not elected. There is, though, a board of governors, 12 Federal Reserve Banks, and the Federal Open Market Committee, the FOMC.

The board of governors consists of seven members nominated by the president and confirmed by the Senate, and they all serve staggered 14-year terms. From among those seven governors, a chair and a vice chair are selected to serve four-year terms. The law requires the chair to be a member of the board of governors, but the president can nominate someone to the board and designate them as chair at the same time. Once confirmed, they serve in both roles.

The outgoing chair is Jerome Powell. He was appointed to the board of governors by President Obama, and President Trump appointed him as chair during his first administration. Powell remained chair through the Biden administration, and his term is up May 15, 2026. The newly confirmed chair is Kevin Warsh. The chair testifies before Congress and serves as the public face of the Federal Reserve.

The 12 regional Federal Reserve Banks act as the Fed's local branches. They supervise banks, handle financial services like payments and cash, and provide insight on regional economic conditions to help guide policy decisions. And most importantly, they actually do the borrowing and lending with the banks.

Then there's the Federal Open Market Committee. When you hear something like the Fed is changing policy, that's the group that's making those decisions. It meets at least eight times per year. It has 12 voting members: the seven governors of the Fed, the president of the New York Federal Reserve Bank, and four other Reserve Bank presidents that rotate over time. This is the group that sets the range for the federal funds rate.

Now, there's a lot of debate over the independence of the Fed. The Fed is supposed to be protected by a moat, free of political influence by the way it is appointed. Governors serve long terms that span multiple administrations, and the Fed funds its own operations in the hope that decisions focus on economic conditions and not election cycles.

That said, the Fed is often a topic of political debate because what it does impacts the economy, and the economy impacts voters, and voters impact, you got it, politicians.

So next time you apply for a car loan, a mortgage, or use a layaway plan, that interest rate is at least partially impacted by the Fed. And now you know just enough to dazzle your friends and neighbors.

Remy: Off to dazzle.

Steve: The Federal Reserve. Just the facts from USAFacts.