Economy

Are credit reporting complaints on the rise?

More and more child labor violations are being reported nationwide, including instances of children working in hazardous occupations. What’s the data behind this trend? What penalties do companies face for violations? Get the facts in this article.

Despite this recent uptick, more minors were involved in child labor violations in 2001 than in any other year in recent history. See the numbers on how things have changed.

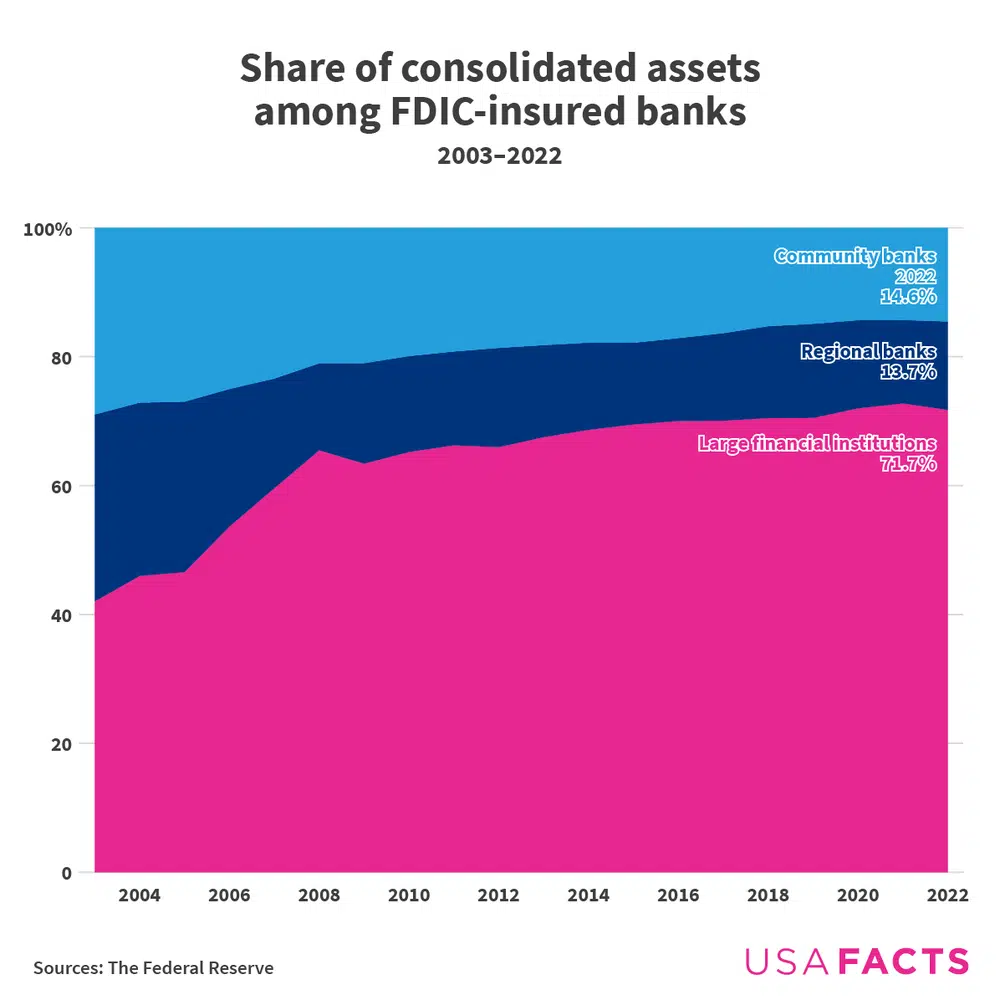

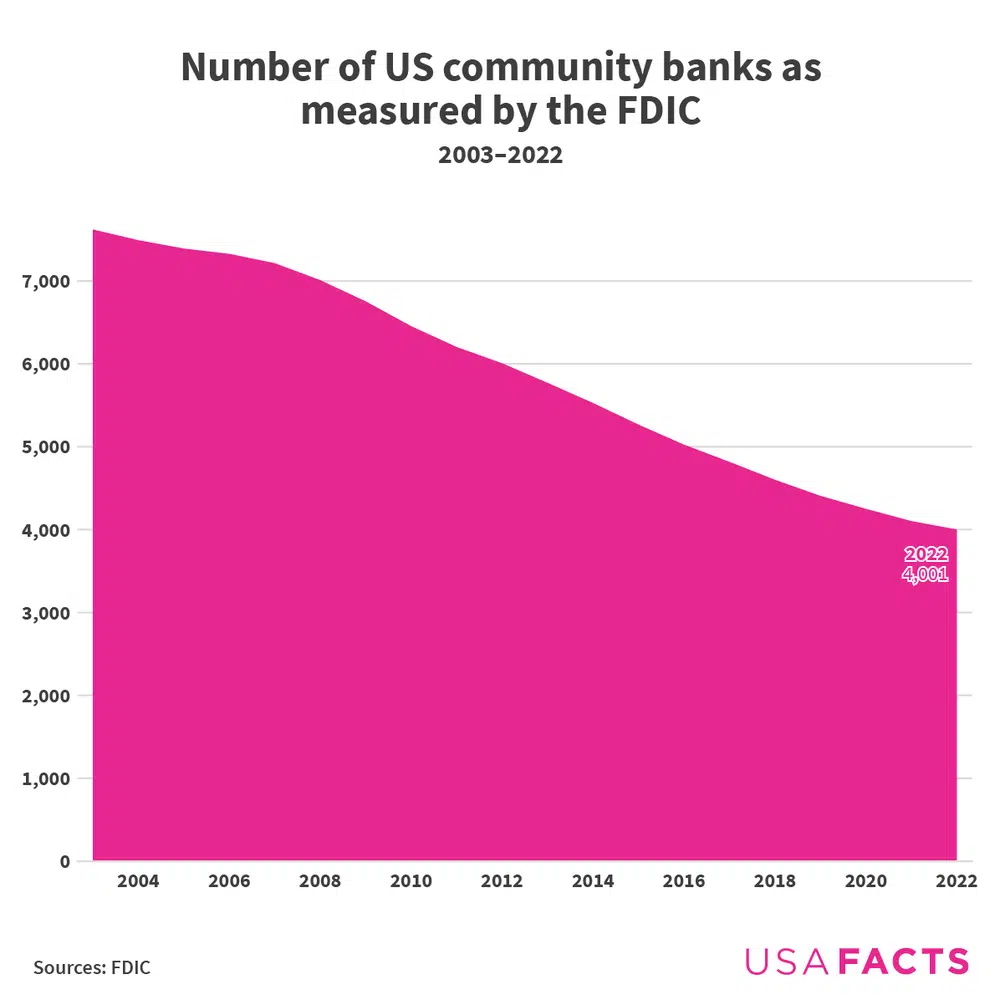

Community and regional banks play a key role in the banking industry, serving local and interstate communities with financial services tailored to their specific needs. However, their market share has been declining while the share of large banks has grown. What are the reasons behind this? Here’s what the data says.

The nation has 4,001 community banks with 27,511 branches and 134 regional banks with 13,109 branches. In contrast, 31 large financial institutions have 30,570 branches nationwide.

Learn more about the role community banks play in American society. Plus, here’s an explanation of bank failures and how often they happen.

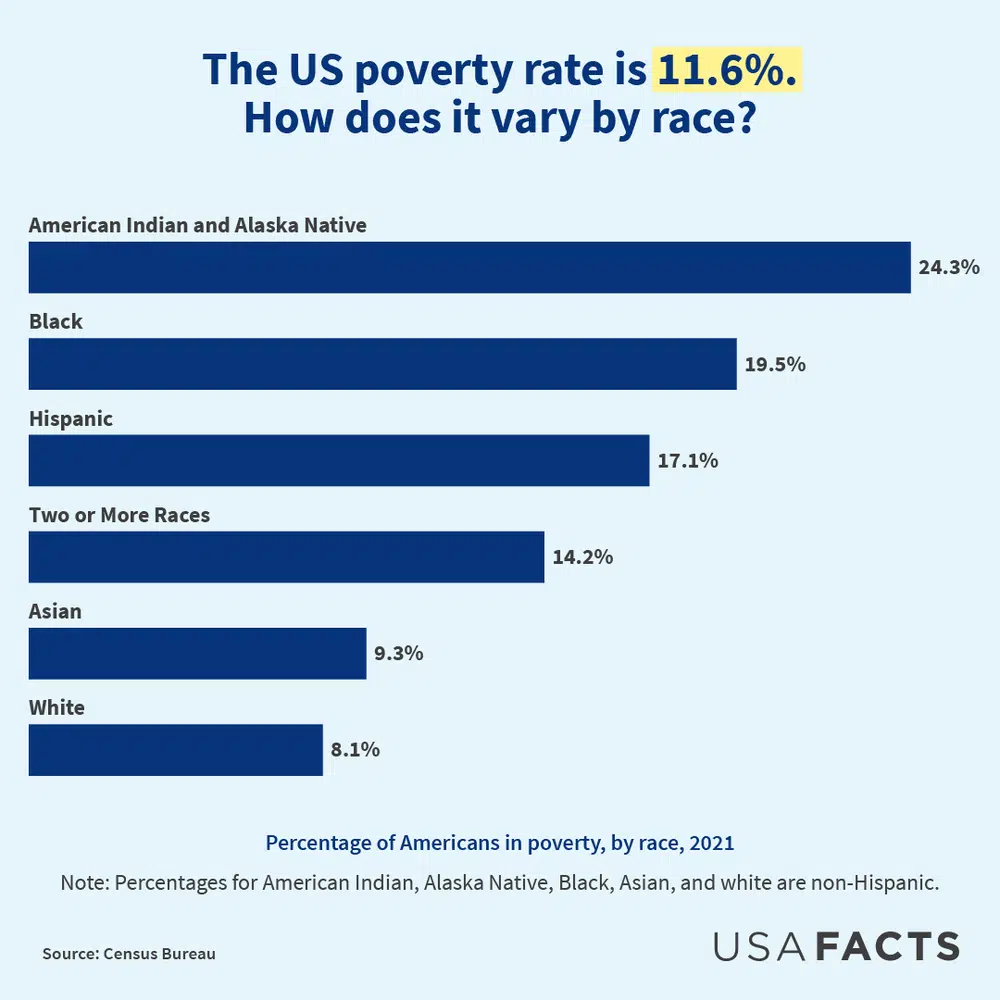

The federal government defines poverty based on family size and income. In 2021, a family of four was considered impoverished if its annual household income was $26,500 or less before taxes. (The median household income for a family of four was $90,657 for 2020–2021.) The government annually adjusts the official poverty measure to account for inflation.

Newsletter

Keep up with the latest data and most popular content.