What is the homeownership rate in the United States?

About 65.9% in 2023. Nearly 2 out of every 3 households owned their home while the remainder rented.

In 2023,

65.9%

of households owned their home

In 2023,

2 in 3

households owned their home

According to the Census Bureau, understanding homeownership rates can help determine if people’s needs are met by available housing and can inform policy and funding decisions.

US homeownership rates declined from the start of the Great Recession through 2016.

During the housing bubble of the mid-2000s, homeownership rates rose to a peak of 69% in 2004. When the housing bubble popped in 2007 and the Great Recession started, foreclosures increased and there was a shift from owning to renting: the homeownership rate declined through 2016, when it bottomed out at 63.4%. It then began to increase. The homeownership rate in 2023 was up 1.5 percentage points from 2018.

Subscribe to get unbiased, data-driven insights sent to your inbox weekly.

Homeownership rates don’t just shift over time — they also vary across places for many reasons, including economic conditions and demographic characteristics.

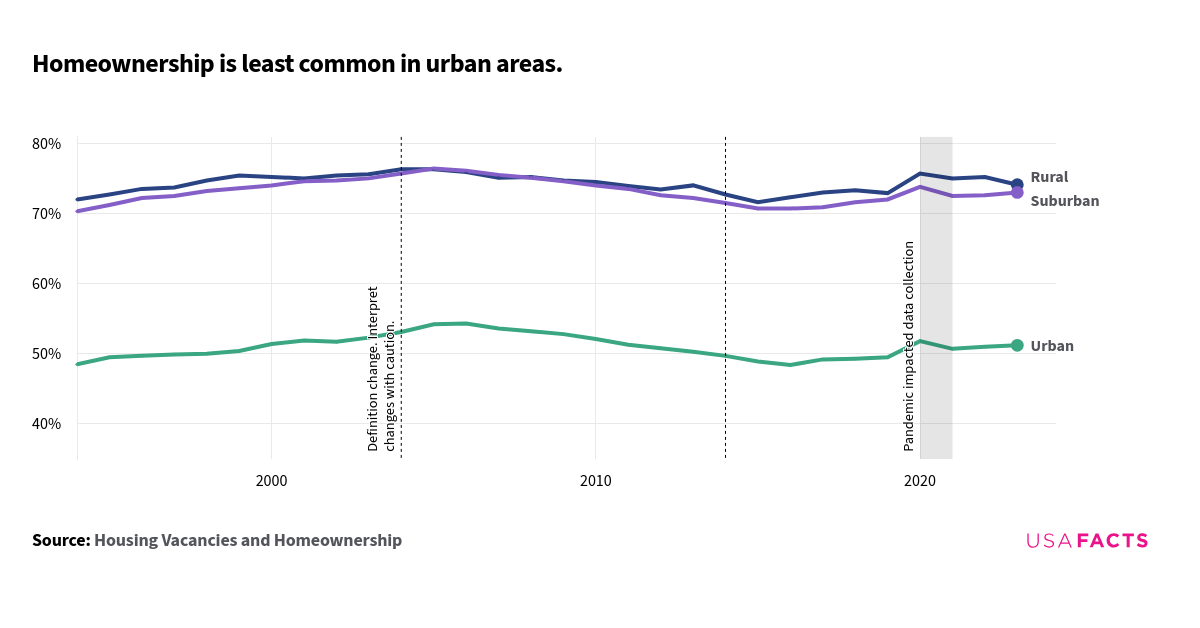

Homeownership is least common in urban areas.

In 2023, homeownership rates were highest in rural areas, at 74.1%; 73.0% of households owned their homes in suburban areas, and 51.2% of households in urban areas. Since their respective housing-bubble highs, homeownership rates have dropped 3.4 percentage points in suburban areas, 3.1 points in urban areas, and 2.2 points in rural areas.

The places defined as rural, suburban, or urban shift every 10 years or so as populations grow, fall, or move and how places more or less economically interconnected. This means changes in the rate may be the result of, for example, a county’s classification changing from rural to suburban as opposed to a real change in homeownership.

State-level homeownership rates also vary due to factors like population density, economic conditions, and population characteristics.

New York had the lowest homeownership rate of any state in 2023.

Homeownership rates ranged from a low of 53.3% in New York to 77% in West Virginia in 2023. Washington, DC’s rate was lower than all states, at least partly due to its entirely urban nature. Washington DC’s 2023 homeownership rate was 40.2%.

Homeownership rate by state (2023)

| 1. | West Virginia | 77% |

| 2. | Delaware | 75.7% |

| 3. | Maine | 75.5% |

| 4. | Mississippi | 75.5% |

| 5. | Wyoming | 74.5% |

| 6. | New Hampshire | 74.3% |

| 7. | Michigan | 74.1% |

| 8. | Minnesota | 74% |

| 9. | Alabama | 73.8% |

| 10. | Vermont | 73.7% |

Change location to see this data for another state.

Methodology

USAFacts standardizes data, in areas such as time and demographics, to make it easier to understand and compare.

The analysis was generated with the help of AI and reviewed by USAFacts for accuracy.

Page sources

USAFacts endeavors to share the most up-to-date information available. We sourced the data on this page directly from government agencies; however, the intervals at which agencies publish updated data vary.