Earned Income Tax Credit (EITC) definition

The Earned Income Tax Credit is a refundable credit for low‑ and moderate‑income workers that lowers their tax bill and can result in a refund.

Published Jan 30, 2026by the USAFacts team

The Earned Income Tax Credit (EITC) is a refundable tax credit that helps low-to moderate-income workers. The EITC reduces the amount of federal income taxes they owe. Some taxpayers can also get a refund, even if they owe no taxes.

To qualify for the Earned Income Tax Credit, taxpayers must:

- Have earned income from working (such as wages, salaries, tips, or self-employment).

- Meet income limits based on filing status and the number of qualifying children they have. (The IRS updates these thresholds each year.)

- Have a valid Social Security number. Spouses and qualifying children must also have Social Security numbers

- File taxes using an allowable status — taxpayers who file as Married Filing Separately are not eligible for the EITC.

- Be a US citizen or resident alien for the entire filing year (or meet certain special rules, if the filer is a nonresident alien).

- Not be claimed as a dependent or qualifying child on someone else’s tax return.

- Have investment income below the annual limit set by the IRS. (This limit is also updated annually).

Meet three criteria, if they do not have a qualifying child:

- Be at least 25 years old but under 65 at the end of the tax year

- Live in the US for more than half the year

- Not qualify as someone else’s dependent

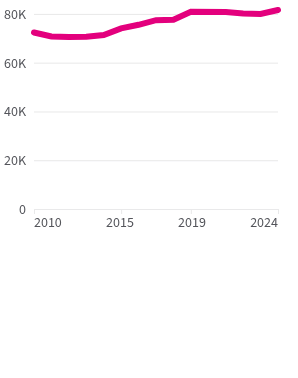

Household income

The median household income in the US was about $82,000 in 2024

What income qualifies as earned income?

Earned income means income received from working, whether it’s from a job or self-employment.

Earned income includes:

- Wages, salaries, tips, and other taxable employee pay

- Net earnings from self-employment or from operating a farm or business

Earned income does not include:

- Investment income (interest, dividends, capital gains)

- Most pensions

- Social security benefits

- Unemployment income